Ever reach the end of the month only to wonder where your hard-earned money actually went? You aren’t alone. For millions of people, the gap between payday and the end of the month is filled with “financial fog”—a state of uncertainty where spending feels random and savings feel impossible. This is where a monthly budget template transforms from a simple document into a powerful financial roadmap. A budget template is more than just a list of numbers; it is a strategic framework that allows you to tell your money where to go instead of wondering where it went. Whether you are trying to climb out of debt, save for a first home, or simply stop living paycheck-to-paycheck, the right structure is the first step toward lasting stability.

The Deep Dive: Why a Monthly Budget Template is Your Greatest Financial Asset

Many people shy away from budgeting because they perceive it as a form of restriction—a “financial diet” that prevents them from enjoying life. In reality, the opposite is true. Using a monthly budget template provides the psychological and mathematical freedom to spend without guilt because every dollar has a designated purpose.

The hidden value of a structured budget lies in visibility and accountability. When your finances are tracked in a centralized template, you uncover “leaks”—those recurring $10 subscriptions or daily convenience purchases that quietly erode your wealth. By quantifying these habits, you shift from reactive spending to proactive planning. Without a template, you are managing your life based on your bank balance, which is a lagging indicator; a budget is a leading indicator, telling you what is possible before you spend the money.

Furthermore, a consistent budgeting process creates an audit trail of your financial behavior. This data is invaluable when you want to scale your lifestyle or prepare for emergencies. The risk of avoiding a template is not just a lack of savings, but the increased stress and anxiety that accompany financial unpredictability. When an unexpected car repair or medical bill hits, a person with a budget sees a manageable hurdle; a person without one sees a crisis.

Anatomy of a Perfect Monthly Budget Template

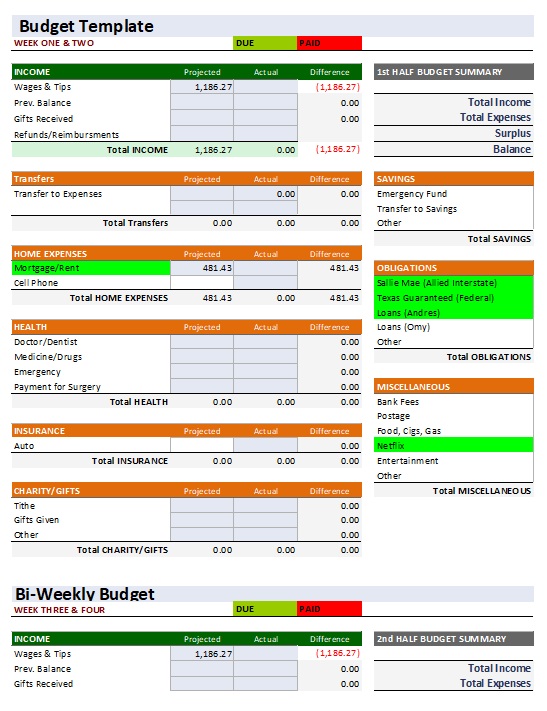

Not all templates are created equal. To move from basic tracking to true financial mastery, your monthly budget template must contain specific components that capture the full picture of your cash flow. A high-quality template should be divided into the following core sections:

- Net Income Stream: This section must list all sources of income after taxes (take-home pay). Include primary salaries, side hustle earnings, dividends, or government benefits.

- Fixed Expenses (Needs): These are non-negotiable costs that rarely change month-to-month.

- Housing (Rent/Mortgage)

- Utilities (Electricity, Water, Internet)

- Insurance (Health, Auto, Life)

- Minimum Debt Payments (Student loans, Credit cards)

- Variable Expenses (Wants/Lifestyle): Costs that fluctuate based on behavior.

- Groceries and Dining Out

- Entertainment and Hobbies

- Fuel and Transportation

- Personal Care and Shopping

- Financial Goals (Savings & Investments): This is where you pay yourself first.

- Emergency Fund contributions

- Retirement accounts (401k, IRA)

- Specific goal buckets (Vacation, House deposit)

- The Variance Column: A critical but often overlooked feature. This column compares your Planned spending against your Actual spending, showing you exactly where you over- or under-spent.

- The Zero-Balance Summary: A final calculation ensuring that Income minus Expenses/Savings equals Zero. This ensures every single cent is accounted for.

Download Free Monthly Budget Template

Step-by-Step Guide: How to Customize and Use Your Monthly Budget Template

Owning a template is only half the battle; the magic happens in the execution. Follow this chronological workflow to maximize the effectiveness of your monthly budget template.

Step 1: The Pre-Month Setup (The Blueprint)

Do not wait until the 1st of the month to start. During the last few days of the previous month, open your template and input your expected income. Based on your goals, allocate funds to your fixed expenses first, then your savings goals, and finally your variable spending. This is your “Plan of Attack.”

Step 2: The Weekly Pulse Check (The Tracking)

A budget is not a “set it and forget it” tool. Set a weekly appointment—perhaps every Sunday afternoon—to input your actual spending from the past seven days. Update the “Actual” column in your template. This prevents the overwhelming task of sorting through 30 days of receipts at once and allows you to pivot your spending if you’ve already hit your dining-out limit by the 15th.

Step 3: The End-of-Month Review (The Optimization)

At the end of the month, analyze your variance. If you consistently overspend on groceries but underspend on entertainment, adjust the categories for the following month. This iterative process refines your accuracy and helps you develop a realistic understanding of your cost of living.

Step 4: Rollovers and Adjustments

If you have a surplus at the end of the month, don’t just leave it in your checking account. Move that “extra” money into your high-yield savings account or toward a high-interest debt payment immediately.

Best Practices & Common Mistakes to Avoid

To get the most out of your monthly budget template, consider these professional tips:

- Automate Where Possible: Use apps that sync with your bank to pull data into your template, or set up automatic transfers to your savings categories so you aren’t tempted to spend that money.

- The “Buffer” Category: Always include a “Miscellaneous” or “Oops” category of $50–$100. No month is perfect, and a small buffer prevents the entire budget from collapsing when a small, unexpected expense arises.

Avoid these common pitfalls:

- Overcomplicating Categories: Don’t create 50 different categories. Group them (e.g., “Home” instead of “Lightbulbs, Soap, Paper Towels”). Too much detail leads to burnout.

- The “All-or-Nothing” Mentality: If you overspend in week two, don’t abandon the template for the rest of the month. A budget is a guide, not a prison. Simply adjust your remaining categories and keep moving forward.

Frequently Asked Questions About Using a Monthly Budget Template

How do I start a monthly budget if my income is irregular?

If you are a freelancer or commission-based worker, use a monthly budget template based on your “lowest likely” income month. Create a “Hill and Valley” fund; during high-income months, save the excess in a separate account. During low-income months, draw from that fund to cover your baseline expenses, ensuring your lifestyle remains stable regardless of the paycheck variance.

What is the 50/30/20 rule in budgeting?

The 50/30/20 rule is a popular framework that can be integrated into any monthly budget template. It suggests allocating 50% of your take-home pay to Needs (housing, utilities, basic food), 30% to Wants (hobbies, dining out, streaming services), and 20% to Financial Goals (debt repayment, savings, investments). It is an excellent starting point for those who aren’t sure how much they should be spending in each category.

How often should I update my budget?

For maximum effectiveness, you should update your tracking weekly. While some people prefer daily logging, weekly updates provide a balanced view of your spending trends without becoming a tedious chore. The most important part is the monthly review, where you set the strategy for the next 30 days.

What happens if I overspend in one category?

This is where the flexibility of a monthly budget template shines. Use a technique called “Budget Shifting.” If you spend $50 too much on car repairs, subtract $50 from your “Entertainment” or “Dining Out” category for the remainder of the month. This keeps your total bottom line intact without requiring you to dip into your emergency savings.

Conclusion: Take Control of Your Financial Future Today

Financial peace of mind doesn’t come from earning more money; it comes from managing the money you have with intention. By implementing a structured monthly budget template, you move from a state of financial chaos to one of absolute clarity. Stop guessing and start growing—download or create your template today, map out your next 30 days, and take the first definitive step toward the lifestyle you deserve.