The transition from a steady paycheck to a fixed income is one of the most daunting psychological and financial shifts an adult will ever experience. For many, the fear isn’t necessarily a lack of savings, but the fear of the unknown: Will my money last? Am I spending too much on travel? How do I handle an unexpected medical crisis without draining my portfolio?

The Deep Dive: Why a Dedicated Retirement Budget Template is Non-Negotiable

Many retirees make the mistake of using the same budgeting logic they employed during their working years. However, retirement introduces unique financial variables—such as Required Minimum Distributions (RMDs), fluctuating healthcare costs, and the absence of employer-sponsored benefits—that make a standard monthly budget insufficient.

The hidden value of using a dedicated retirement budget template lies in its ability to provide predictive clarity. Without a formalized system, you are prone to “lifestyle creep,” where the excitement of newfound free time leads to unplanned spending that erodes your principal balance. A template forces accountability, ensuring that every dollar is aligned with your goals, whether that is leaving a legacy for your grandchildren or traveling the world.

Beyond the benefits, the risks of neglecting a formal budget are severe. “Sequence of Returns Risk”—the danger of a market downturn occurring early in your retirement—can be catastrophic if you are withdrawing funds blindly. A template allows you to build in “buffer zones” and adjust your spending dynamically based on market performance, effectively insulating your lifestyle from economic volatility. In short, it transforms your financial plan from a static guess into a living, breathing strategy.

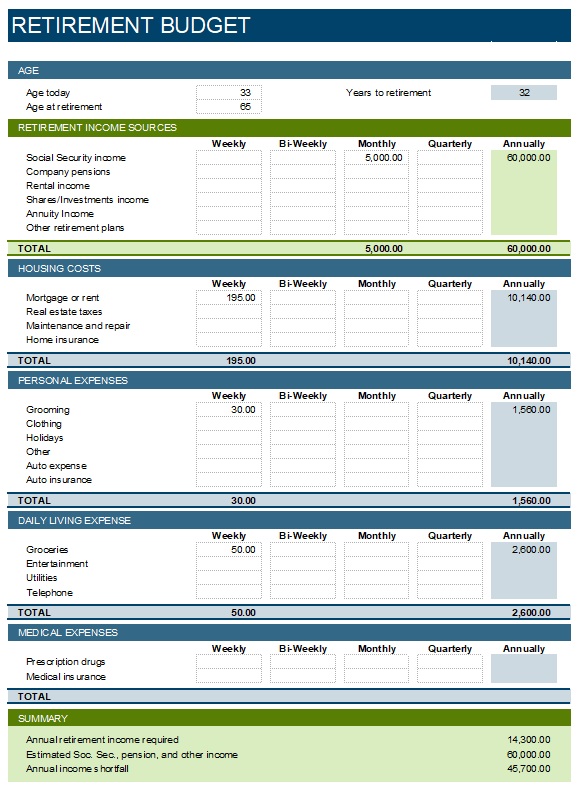

Anatomy of a Perfect Retirement Budget Template

Not all spreadsheets are created equal. To truly capture the complexity of post-career life, your retirement budget template must go beyond simple “Income vs. Expenses.” A professional-grade template should be divided into the following core components:

1. Diversified Income Streams

- Guaranteed Income: Social Security benefits, pensions, and annuities.

- Variable Income: Dividend payouts, rental income, or part-time consulting fees.

- Portfolio Withdrawals: Scheduled draws from 401(k)s, IRAs, or brokerage accounts (including a section for RMDs).

2. Essential “Must-Have” Expenses

- Housing: Mortgage/rent, property taxes, home insurance, and maintenance.

- Healthcare: Medicare premiums, supplemental insurance, out-of-pocket prescriptions, and long-term care premiums.

- Utilities: Electricity, water, gas, internet, and phone.

- Groceries & Basic Transport: Essential fuel, car insurance, and nutrition.

3. Discretionary “Nice-to-Have” Spending

- Leisure & Travel: Vacation funds, dining out, and hobbies.

- Entertainment: Streaming services, club memberships, and books.

- Gifting: Holiday presents and charitable donations.

4. The Safety Net & Tax Reserve

- Emergency Fund: A dedicated liquid cash reserve for unplanned repairs or crises.

- Tax Liability: A calculated set-aside for taxes on taxable withdrawals to avoid a surprise bill in April.

- Inflation Adjustment: A percentage-based increase applied annually to maintain purchasing power.

Download Free Retirement Budget Template

Step-by-Step Guide: How to Customize and Use Your Template

A template is only as effective as the data entered into it. To maximize the utility of your retirement budget template, follow this chronological workflow:

- The Baseline Audit: Before filling in the template, gather 12 months of bank and credit card statements. Categorize your spending to understand your current “burn rate.” This prevents you from underestimating your actual costs.

- Project Your Income: Input your guaranteed monthly sums first. Then, determine your “Safe Withdrawal Rate” (e.g., the 4% rule) from your investments to fill the gap between your guaranteed income and your baseline expenses.

- Stress-Test the Scenario: Create three versions of your budget: a Conservative version (essential spending only), a Balanced version, and an Optimistic version (including luxury travel). This prepares you for market volatility.

- Establish a Review Cadence: Do not set it and forget it. Update your retirement budget template monthly to track actual vs. projected spending. Perform a “Deep Review” quarterly to adjust for inflation or changes in investment returns.

- Automate the Flow: Whenever possible, set up automatic transfers from your investment accounts to your spending account on a specific date, mirroring the “paycheck” feel to maintain psychological comfort.

Best Practices & Common Mistakes to Avoid

To get the most out of your financial tracking, consider these professional tips:

- Prioritize Digital Over Paper: While a printable log is nice, a digital template (Excel or Google Sheets) allows for automatic calculations and “what-if” scenario modeling that paper cannot provide.

- Don’t Forget “Lumpy” Expenses: Many people forget annual expenses like car registration or home insurance. Divide these annual costs by 12 and include them as a monthly expense to avoid cash-flow shocks.

- Avoid Over-Categorization: If your template has 50 different categories, you will stop using it. Group expenses into broad buckets (e.g., “Wellness” instead of “Gym, Pharmacy, Dental, Massage”) to keep the process sustainable.

- Always Backup Your Data: Ensure your budget is stored in a secure cloud environment and share the access link with a trusted spouse or legal representative.

Retirement Budgeting: Frequently Asked Questions

How often should I update my retirement budget template?

While you should track expenses daily or weekly, a full reconciliation of your retirement budget template should happen monthly. This allows you to spot trends—such as a spike in utility costs or overspending on dining—and pivot your spending for the following month before it impacts your long-term portfolio.

What is a “Safe Withdrawal Rate” and how does it fit into a template?

The Safe Withdrawal Rate (SWR) is the percentage of your total portfolio you can withdraw annually without running out of money over a 30-year period. In your template, this is the figure that determines your “Variable Income” line. While 4% is the traditional benchmark, many modern planners suggest 3% to 3.5% depending on current market valuations.

Should I include a “buffer” or “slush fund” in my retirement budget?

Absolutely. A rigid budget is a fragile budget. Your retirement budget template should include a “Miscellaneous” or “Buffer” line item (typically 5-10% of total spending). This prevents you from feeling like you’ve “failed” your budget when a small, unplanned expense arises.

How do I handle taxes within a retirement budget?

Taxes are often the most overlooked part of retirement planning. If you are withdrawing from a Traditional IRA or 401(k), those funds are taxable. Your template should show the gross withdrawal and then subtract a percentage for taxes, leaving you with the net amount available for spending.

Conclusion: Take Control of Your Future Today

Financial peace of mind in retirement doesn’t come from having a mountain of money—it comes from knowing exactly how that money is working for you. By implementing a comprehensive retirement budget template, you replace uncertainty with a strategy. Don’t leave your legacy to chance; start auditing your expenses and mapping your income today to ensure your golden years are truly golden.