For many students, the transition to higher education is the first time they encounter the “financial shock” of adulthood. Between skyrocketing tuition, unpredictable textbook costs, and the siren call of daily takeout, it is incredibly easy for a bank account to hit zero long before the semester ends. This is where a student budget template becomes more than just a spreadsheet—it becomes a survival tool. A student budget template is a structured financial framework designed to track income, categorize expenses, and allocate funds toward both immediate needs and future goals, ensuring that academic success isn’t derailed by financial instability.

The Deep Dive: Why a Student Budget Template is Non-Negotiable for Academic Success

Many students make the mistake of “mental budgeting,” where they glance at their balance and decide if they can afford a dinner out. However, this approach ignores the “invisible” costs of student life—the quarterly lab fees, the annual subscription renewals, and the inevitable emergency repair. Using a dedicated student budget template transforms your relationship with money from reactive to proactive.

The hidden value of a structured budget lies in psychological liberation. When you have a clear map of where every dollar is going, the chronic anxiety of “Do I have enough?” disappears. This cognitive load reduction allows you to focus your mental energy on your studies rather than your bank balance. From a practical standpoint, a budget provides an audit trail of your spending habits. It reveals patterns—such as that $60-a-month habit on streaming services you forgot to cancel—allowing you to reclaim leaked funds.

The risks of avoiding a budget are severe. Without a system, students often fall into the “credit card trap,” using high-interest loans to cover basic living expenses. This creates a cycle of debt that can haunt graduates for a decade. By implementing a template today, you aren’t just managing money; you are building the financial literacy skills that separate successful professionals from those who struggle with paycheck-to-paycheck living long after graduation.

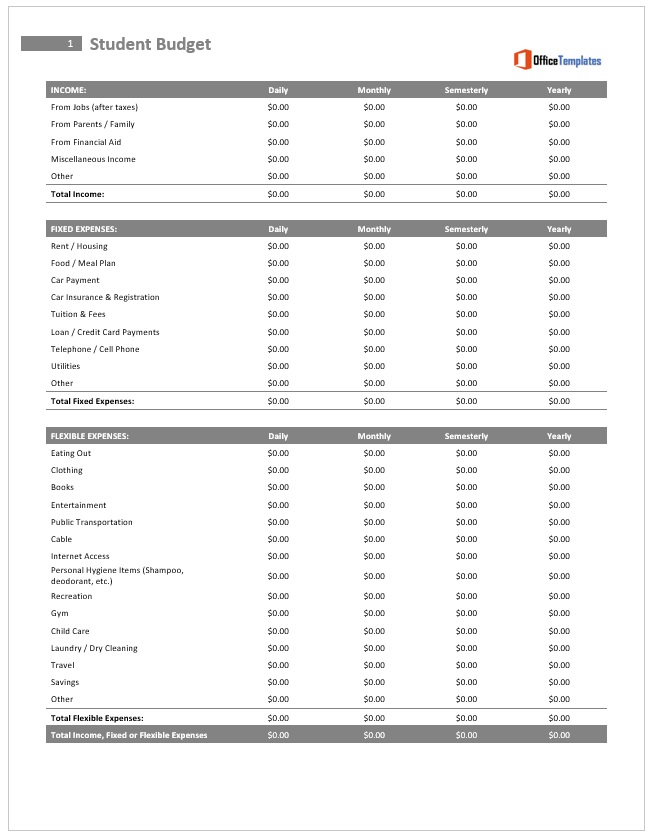

Anatomy of a Perfect Student Budget Template: Essential Components

Not all templates are created equal. To be truly effective, your student budget template must capture a 360-degree view of your financial ecosystem. Whether you are building one in Excel, Google Sheets, or using a physical planner, ensure it contains these five critical sections:

- Income Streams (The Inflow): Do not just list a single number. Break down your income by source.

- Student loans/grants (distributed by semester).

- Part-time job wages (net pay after taxes).

- Parental contributions or stipends.

- Scholarships and bursaries.

- Fixed Expenses (The Non-Negotiables): These are costs that remain constant every month.

- Rent/Dorm fees.

- Insurance (Health, Renter’s, Auto).

- Internet and phone plans.

- Fixed subscription services.

- Variable Expenses (The Flex Zone): These fluctuate and are the primary areas where you can cut costs.

- Groceries and dining out.

- Transport (Gas, Uber, Public Transit).

- Textbooks, software, and school supplies.

- Social activities and entertainment.

- Savings & Debt Repayment: A section dedicated to your future self.

- Emergency fund (aiming for $500–$1,000 initially).

- Credit card minimum payments.

- Small-scale investments or “fun money” savings.

- The Variance Column (Budget vs. Actual): This is the most important part of any student budget template. It allows you to compare what you planned to spend against what you actually spent, highlighting exactly where your budget leaked.

Download Free Student Budget Template

Step-by-Step Guide: How to Customize and Use Your Student Budget Template

Having a template is only half the battle; the magic happens in the execution. Follow this chronological workflow to ensure your financial plan stays accurate and actionable.

- The Baseline Audit (Month 0): Before filling out your template, look at your bank statements from the last three months. Categorize every expense to find your “average” spending. This prevents you from setting unrealistic goals that lead to burnout.

- Set Your Monthly Allocation: At the start of each month, enter your expected income. Subtract your fixed expenses first, then allocate funds to your savings goals. Finally, divide the remainder among your variable categories (Groceries, Fun, etc.).

- The Weekly Check-In: Budgeting is not a “set it and forget it” task. Every Sunday, spend 15 minutes updating your student budget template. Enter your actual spending for the week. This prevents a “month-end surprise” where you realize you overspent in the first ten days.

- The Monthly Pivot: At the end of the month, analyze your Variance Column. If you consistently overspend on “Dining Out” but underspend on “Books,” shift those funds in next month’s template. This is called “dynamic budgeting,” and it ensures your plan evolves with your lifestyle.

- Seasonal Adjustments: Remember that student life is cyclical. Increase your budget for “Supplies” in September and January, and perhaps increase “Entertainment” during the summer break.

Best Practices & Common Mistakes to Avoid

To maximize the efficiency of your student budget template, embrace automation. Link your template to a digital banking app or use a shared Google Sheet so you can update your spending on the go. Manual entry is the primary reason students abandon budgeting; the easier it is to track, the more likely you are to stick with it.

Avoid these common pitfalls:

- Over-Categorization: Don’t create 50 different categories. If you have “Coffee,” “Snacks,” and “Lunch” as separate lines, you’ll spend more time managing the sheet than spending the money. Group them under “Food & Drink.”

- The “Perfect Budget” Fallacy: Don’t aim for a zero-dollar variance. Life happens. Allow for a small “Miscellaneous” buffer (e.g., $20–$50) to handle unexpected costs without feeling like you’ve “failed” your budget.

- Ignoring Small Leaks: A $5 subscription seems negligible, but across ten services, it’s a significant monthly drain. Track everything.

Frequently Asked Questions About Student Budgeting

How often should I update my student budget template?

For the best results, you should record your transactions weekly. While a monthly review is necessary for long-term planning, weekly updates prevent you from losing track of small cash purchases and allow you to adjust your spending in real-time before the month ends.

What is the best app or software to use for a student budget template?

The “best” tool is the one you will actually use. For those who love data and customization, Google Sheets or Microsoft Excel are superior because they offer total control. For those who prefer automation, apps like YNAB (You Need A Budget) or Mint are excellent, as they sync directly with bank accounts.

How do I handle irregular income, like freelance work or occasional gifts?

When using a student budget template with irregular income, use a “conservative estimate.” Budget based on the minimum amount you know you will receive. When a “bonus” or larger-than-expected payment arrives, allocate it immediately to your savings or debt repayment rather than increasing your lifestyle spending.

What should I do if I consistently overspend my budget?

If you are consistently over budget, it is usually a sign of one of two things: your goals are too restrictive, or you have a “spending leak.” Review your variable expenses and identify the “want” vs. the “need.” If the budget is truly too tight, look for ways to increase income (e.g., a few extra hours of work) or reduce fixed costs (e.g., finding a cheaper phone plan).

Conclusion: Take Control of Your Financial Future

Financial stress is one of the leading causes of student dropout and mental health struggles. By implementing a student budget template, you are taking a decisive step toward stability and independence. Start today by listing your income and expenses—small changes in how you track your money now will lead to massive dividends in your professional life. Your future self will thank you.